Eligibility

To apply, you must meet the following eligibility requirements:

- You must live or work in Thurston County

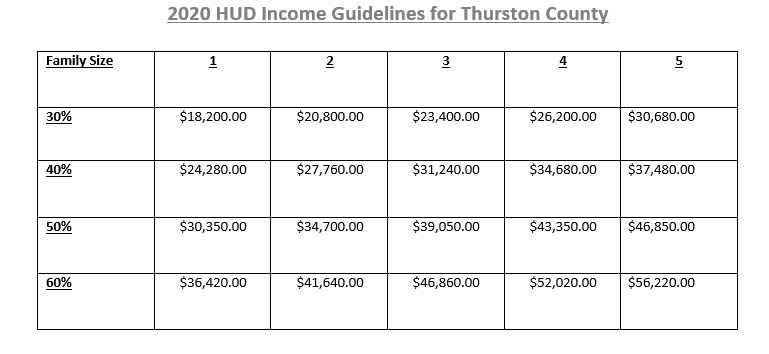

- Your total household income must be within our current household income limits This includes all income from all members of your household.

- In addition to the household income limit, the total income from applicants must be greater than our current minimum threshold. An applicant is a person who wants to participate in the program and own a Habitat home.

- You must be a citizen or legal permanent resident of the United States

- You must not have filed bankruptcy in the last year, and if you have filed bankruptcy in the last two years, your bankruptcy must be discharged for at least two years before you close on your home

- You must apply for a house model that we plan to build in the next construction phase

- You must be able to get approved with one of our Zero Equivalency Mortgage partners for a Home Loan

Countable Income

On the application, we ask you to disclose all of your household income (see below for one exception). We ask for all of your household income including non-cash income like food stamps and housing assistance because it helps us understand your monthly budget.

However, not all income will count for eligibility purposes. To determine your eligibility, we only include cash income that we can reasonably expect to last at least three years. Income can be from work, public assistance, retirement, child support, social security, or any other source of cash income. Income from employment is not required. For all income, you must submit sufficient documentation to verify that you receive it.

In general, the following income does not count towards eligibility:

- Non-cash income like food stamps

- Unemployment benefits

- Gift income from relatives or friends

- Certain public programs with limits on the duration of assistance

One Exception

We can count (and often do count) child support, alimony or maintenance support income, but you may ask us to exclude this income in our mortgage underwriting. This is the only source of income you can ask us to exclude if you want to.

Qualifications

Habitat uses three criteria to evaluate applications: housing need, ability to pay, and willingness to partner.

Housing need

This is your reason for applying to the program and why you want to be a Habitat homeowner. You might not qualify for a conventional home loan. You might not have enough savings for a down payment. Maybe you simply want to own your own home. Your current housing might be less than ideal. Your home might have repair issues (the most common is mold), or you might pay too much in rent. Most folks have a housing need.

Ability to pay

This is our term for your financial health. Qualified buyers have diverse credit histories. Some have little or no credit. Others have some or decent credit. Most qualified buyers have some debt, like auto loans, student loans or medical debt. Most qualified buyers have little or no debt in collections. Your debt situation doesn’t need to be perfect, but you need to show you’re making your best effort to pay your debts on time.

Willingness to partner

This is our term for participating in the program. Qualified buyers, and other adults in the household, are willing to complete, at minimum, 500 hours of “sweat equity” as well as complete homebuyer education. Qualified buyers are active participants in their homeowners association (HOA).

Lastly, every person 18 years or older who is listed on a program application is required to submit to a background check including a Washington State Patrol criminal history check and National Sex Offender Registry Check.

{kind=link}